7 Surprising Money Lessons for Your 20s to Build Wealth Faster

Discover 7 powerful money lessons for your 20s that help you build wealth faster avoid lifestyle inflation and leverage time investing and skills for financial freedom.

PERSONAL FINANCE

E. O. Francis

1/30/20266 min read

Your 20s aren’t just a decade for figuring life out; they're the most powerful financial advantage you’ll ever have. Yet most people waste these years waiting for a real salary or the perfect moment to start building wealth. That delay quietly costs them freedom, flexibility and hundreds of thousands of dollars over time. The truth is wealth isn’t built by earning more later it’s built by acting earlier. In this guide you’ll discover seven surprising money lessons that flip traditional advice on its head showing you how to use time automation mindset and skill building to grow wealth faster than most people think is possible. If you’re in your 20s and want money to work for you not control you this is where it starts.

1. Why Your 20s Are a Financial Superpower

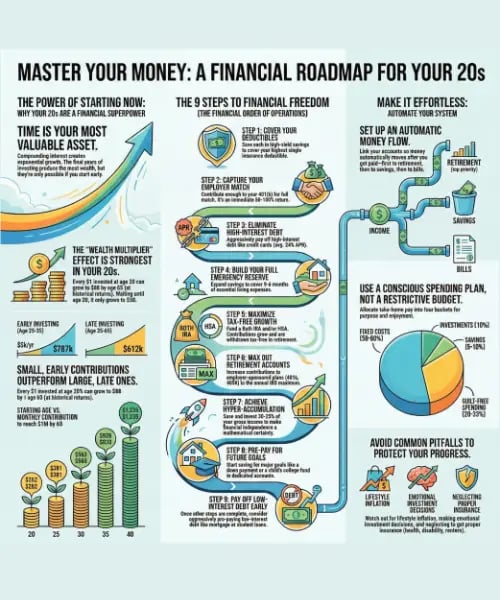

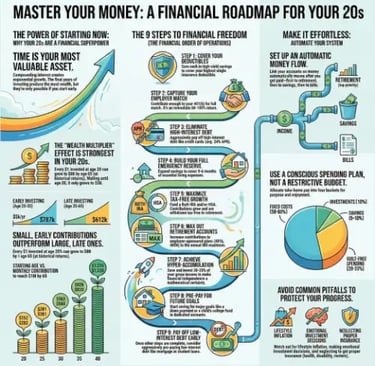

Mastering critical Money Lessons early in your professional life creates a massive advantage for your future security. Many young adults believe they should wait for a high salary before they start building their wealth. This common delay ignores the power of temporal leverage which makes time your most valuable capital asset. Time is a finite resource that allows your invested dollars to grow without any extra manual effort. If you start today, you can harness growth that is almost impossible to replicate in later decades. Waiting even one single decade costs you hundreds of thousands of dollars in potential future security and freedom.

2. The Mathematical Miracle of the Wealth Multiplier

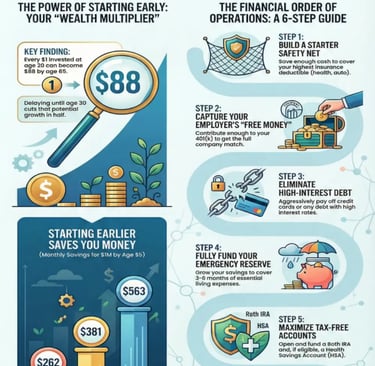

It is a mathematical miracle that a single dollar today carries so much weight for your future self. Every dollar you invest at age 20 carries the potential to grow 88 times by your retirement. This exponential growth occurs because your earnings eventually begin to generate their own earnings over many decades. A younger person contributes much less total principal to reach a million dollars than an older person. Market returns provide the majority of your final portfolio value when you start in your early twenties.

You can use the Rule of 72 to estimate how quickly your initial investments will double in value. An investment with a 7 percent return will double in value approximately every 10 years. This velocity means your money can complete four doubling cycles before you reach age 65. The final doubling cycle between age 55 and 65 produces the most significant absolute growth for your portfolio.

"The earlier you start investing, the harder your dollars can work."

3. Why Automation Beats Willpower Every Single Time

We often overestimate our own willpower, but the reality of our busy lives often gets in the way. The human brain is naturally lazy but programmable because it relies on simple short cuts for daily choices. Choice paralysis often occurs when we face too many individual decisions about how to spend our cash. Automating your finances prevents the dopamine loops that often lead to impulsive spending on unnecessary items. The Next 100 Principle ensures that every new dollar follows a specific path to your financial goals.

To manage your income effectively, you should set up a Conscious Spending Plan with these target categories:

Fixed Costs: 50 to 60 percent of your pay for housing, utilities, and essential bills.

Investments: 10 percent of your take home pay directed toward your future wealth.

Savings Goals: 5 to 10 percent for specific items like travel, weddings, or a home.

Guilt Free Spending: 20 to 35 percent for dining out, hobbies, and pure entertainment.

4. Mastering the Financial Order of Operations (FOO)

You can think of the Financial Order of Operations as a simple math formula for your money. This system acts as a roadmap to ensure you prioritize your dollars for the highest possible efficiency. The order in which you handle your money matters more than the total amount you earn. By following this sequence, you protect yourself from risk while maximizing your future growth potential. You must complete the defensive moves before you begin aggressive wealth building in the market.

Deductibles Covered: Save enough to cover your highest insurance deductible immediately.

Employer Match: Capture every penny of your company match for a guaranteed return.

Predatory Debt: Eliminate expensive debt such as credit card balances as fast as possible.

Emergency Reserves: Build a fund that covers three to six months of living expenses.

Roth and HSA: Maximize these accounts to take full advantage of tax exempt growth.

Step One acts as the psychological floor for your entire financial roadmap. By covering your insurance deductibles first, you create a buffer against sudden and unexpected life events. This shield protects the free money you gain from your employer match in Step Two. Without this cash reserve, you might be forced to use predatory credit card debt in Step Three. This tactical sequence manages your risk so your wealth growth never has to stop for a crisis.

5. Rewriting Your Inherited Money Scripts

Many people enter their professional lives with unconscious money scripts they absorbed during their childhood years. These beliefs determine how you treat your income and how you react to your growing debt. An avoidant attachment style often makes people fear looking at their own bank statements or monthly bills. Shifting to a secure attachment style allows you to manage your capital with total confidence and clarity. Moving toward an internal locus of control is more important for your wellness than your current salary.

You should also challenge common myths that prevent you from seeking a life of financial abundance. Many people incorrectly claim that money is the root of all evil in our world. The actual quote states that the love of money is the root of all evil. Money itself is merely a neutral tool and a resource for your personal freedom. When you treat money with respect, it is more likely to stay and grow for you. You have the power to challenge your internal programming and create a new future today.

6. Escaping the Trap of the Golden Handcuffs

Lifestyle inflation is a common trap where your spending rises at the same rate as your income. As you earn more, your former luxuries quickly begin to feel like absolute necessities in your mind. This cycle forces you to stay in jobs you may hate just to pay for things. You become trapped by golden handcuffs that limit your career choices and your personal autonomy. To avoid this, you should follow the 10 percent rule for every raise you receive.

Living like a resident for several years after graduation can create a permanent and massive financial advantage. This strategy allows you to aggressively eliminate debt and build a stable foundation for your wealth. You should focus on making money make a difference instead of letting it change who you are. True wealth is about having the power to choose how you spend your limited time. We should use our resources to build a life that aligns with our deepest values.

"I like when money makes a difference but doesn't make you different."

7. Skill Stacking for Unlimited Human Capital

Human capital represents the discounted present value of all the future earnings you will generate while working. This is your most valuable asset during the third decade of your life. Skill stacking involves combining two average skills to create a rare and highly valuable career profile. For example, combining coding skills with public speaking makes you a rare and highly valuable professional. This combination allows you to charge more for your time and expertise in the open market.

Artificial intelligence implementation and data science are high earning skills that will dominate the upcoming professional landscape. Persuasive copywriting and strategic communication also remain essential for leaders who want to maximize their income. Mastering salary negotiation is another way to increase your human capital with very little extra work. Negotiating a 5,000 dollar increase in your starting salary can result in 500,000 dollars over your career. Small wins in your early twenties result in massive payouts by the time you retire.

Conclusion: Your Abundance Cycle Starts Today

These seven money lessons provide a complete roadmap for building your wealth while you are still young. Financial freedom is about having the power to choose how you spend your very limited time. You can start your own abundance cycle today by making small and automated changes to your habits. Focus on the mathematical power of your time and the efficiency of the financial order. Secure your future by mastering your human capital and avoiding the trap of lifestyle inflation. If you treated your money like a life partner, would it choose to stay or leave today?