Stop Losing Value: 2026’s Top Assets That Outperform and Protect Better Than Bank Cash

Discover the top assets for 2026 that outperform bank savings and protect your money from inflation. Learn smarter alternatives to cash and low-interest accounts.

FINANCE & INVESTING

E. O. FRANCIS

2/3/20264 min read

For decades, cash was marketed as safety. In 2026, it is increasingly understood as silent risk.

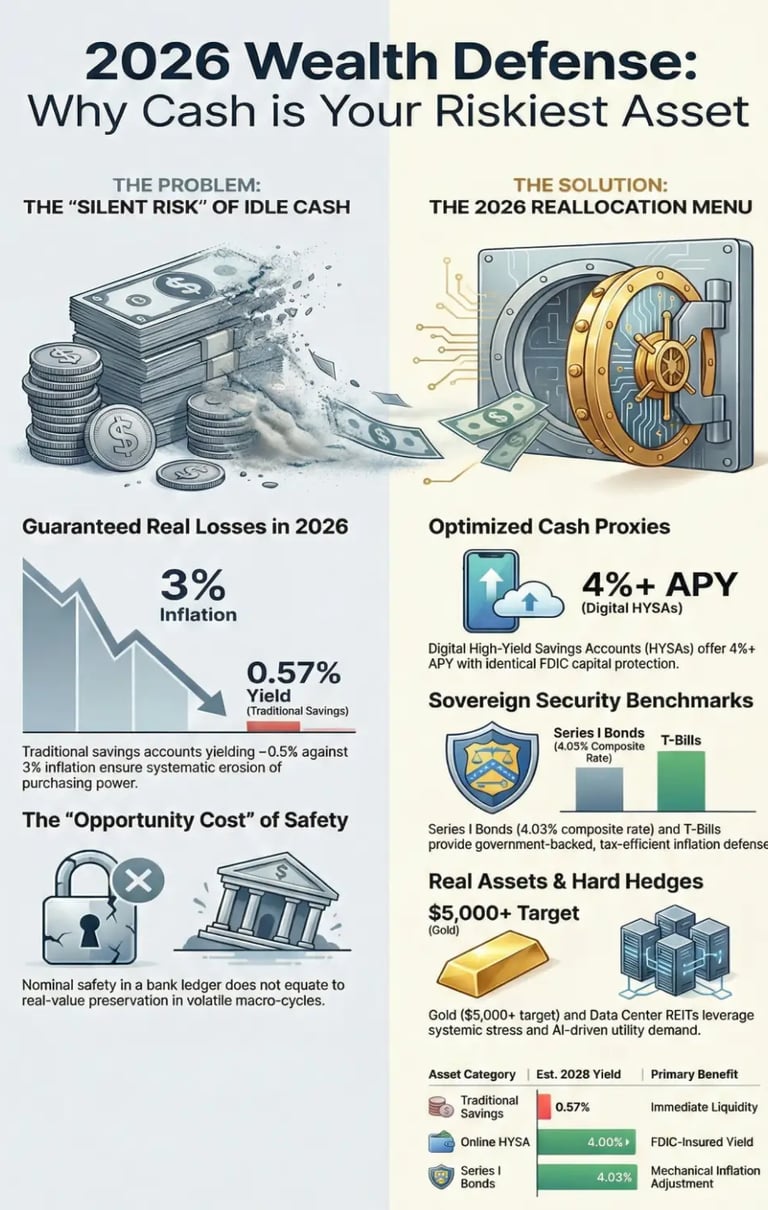

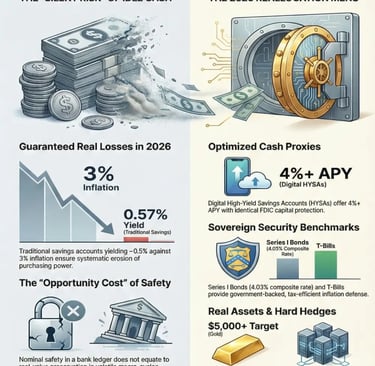

While banks advertise “growth” through interest, the truth is harsher. Cash is a wasting asset in inflationary regimes. Even modest inflation compounds against savers, eroding purchasing power year after year. A savings account yielding 0.5 percent in a 3 percent inflation environment guarantees a real loss. This is not conservatism. It is controlled decay.

As fiscal deficits expand, monetary cycles shorten, and geopolitical risk remains elevated, capital allocators are shifting away from idle cash and toward yielding, inflation aware, and utility backed assets. The objective is no longer just preservation, but real value defense with upside optionality.

Below are the asset classes sophisticated investors are prioritizing in 2026 to outperform bank cash while maintaining liquidity, security, and resilience.

1. Optimized Cash Proxies: Liquidity Without Value Destruction

Cash still has a role, but only when optimized.

Traditional savings accounts, typically yielding below 1 percent, are structurally incapable of preserving real value. By contrast, modern cash proxies offer liquidity while narrowing or even eliminating the inflation gap.

High Yield Savings Accounts (HYSAs):

Fintech and digital banks now routinely offer 4 percent or higher APY, often with full FDIC insurance up to statutory limits. This represents a meaningful upgrade. Identical capital protection, superior yield, and zero duration risk. In a volatile macro environment, HYSAs function as defensive cash buffers rather than wealth drains.

Money Market Funds (MMFs):

MMFs invest in short duration, high quality instruments such as Treasury bills and commercial paper. While not FDIC insured, they benefit from diversification, daily liquidity, and rapid repricing when interest rates rise. For institutional allocators, MMFs are often preferred as operational cash vehicles due to yield responsiveness.

Key insight: In 2026, unoptimized cash is a liability. Optimized liquidity is a strategic asset.

2. Sovereign Security: Government Backed Value Storage

When capital seeks certainty, it gravitates toward sovereign guarantees.

Treasury Bills (T Bills):

Short term Treasuries offer competitive yields with near zero credit risk. Their exemption from state and local taxes materially improves after tax returns, particularly for high earners. For capital with a defined short term horizon, T Bills represent one of the most efficient risk adjusted stores of value.

Series I Savings Bonds:

Bonds are explicitly engineered for inflation protection. Their composite rate structure ensures that purchasing power adjusts alongside CPI, making them one of the few instruments that mechanically defend real value. For conservative investors, they function as inflation insurance with government backing.

Treasury Inflation Protected Securities (TIPS):

TIPS adjust principal in response to inflation, providing institutional grade protection against unexpected price shocks. While subject to market volatility, they are highly effective within diversified portfolios as inflation ballast.

Key insight: Sovereign debt is not about excitement. It is about certainty when confidence in fiat purchasing power weakens.

3. Precious Metals: Insurance Against Systemic Stress

Gold and silver do not generate cash flow. That is precisely their strength.

They exist outside the credit system, immune to counterparty risk, and resistant to monetary debasement. In periods of institutional stress, metals serve as financial insurance, not speculative assets.

Gold:

Gold’s role as a reserve asset is strengthening, not fading. Central banks continue to accumulate it as a hedge against currency volatility. Historically, gold performs best during easing cycles, geopolitical uncertainty, and declining real rates, all conditions expected to persist into 2026.

Silver:

Silver adds an industrial growth component. Its use in renewable energy, electronics, and medical applications introduces a demand floor that complements its monetary hedge characteristics. Though more volatile, silver offers asymmetric upside during reflationary periods.

Key insight: Precious metals are not alternatives to productive assets. They are protection against monetary error.

4. Real Assets: Income Anchored to Physical Demand

Unlike financial abstractions, real assets derive value from human necessity.

Income Producing Real Estate:

Property benefits from scarcity, utility, and inflation pass through via rent adjustments. In inflationary environments, replacement costs rise, reinforcing asset value. Well located real estate remains one of the most durable wealth building vehicles over multi decade horizons.

REITs:

For investors seeking liquidity and diversification, REITs provide exposure without operational burden. Their mandatory dividend distribution creates reliable income streams.

2026 Focus Areas:

Healthcare REITs benefit from demographic inevitability.

Data Center REITs underpin the digital and AI economy, making them infrastructure plays rather than speculative technology bets.

Key insight: Assets tied to shelter, health, and data tend to outlast cycles.

5. Quality Equities: Ownership Over Exposure

Cash is a claim on currency. Stocks are a claim on productive enterprise.

Dividend Kings:

Companies with decades long dividend growth histories demonstrate pricing power, operational discipline, and resilience. These firms often outperform inflation over full cycles while providing dependable income.

AI Margin Expansion:

The most compelling equity opportunities in 2026 are not speculative AI startups, but established companies leveraging AI to reduce costs, improve efficiency, and expand margins. These productivity gains translate directly into earnings growth and shareholder returns.

Key insight: In inflationary eras, ownership beats lending.

6. Alternative Income: Structured Yield Without Equity Volatility

As investors search for yield beyond traditional bonds, structured income strategies are gaining relevance.

Private Credit and Senior Loans:

Floating rate structures benefit from elevated interest rates while sitting higher in capital stacks. When underwritten conservatively, they offer attractive yield with controlled risk.

Infrastructure Assets:

Toll roads, utilities, and energy transport systems generate predictable cash flows tied to real economic usage rather than market sentiment.

Key insight: Cash flow anchored to usage outperforms promises tied to policy.

Strategic Allocation Framework for 2026

Capital protection is not about choosing a single asset. It is about intentional allocation.

Liquidity needs to dictate duration.

Inflation expectations dictate asset selection.

Tax positioning dictates net outcomes.

For short term certainty, optimized cash and Treasuries dominate.

For medium term resilience, real assets and inflation linked securities matter.

For long term growth, equities and productivity driven businesses remain unmatched.

Final Thought

In 2026, the greatest risk is not volatility. It is complacency.

Leaving capital idle in low yield cash is no longer conservative. It is a guaranteed loss strategy in real terms. Wealth preservation today requires movement into assets that yield, adapt, and endure.

Smart money is not fleeing risk.

It is fleeing erosion.