What is the FIRE Financial Theory?

What is the FIRE financial theory? Discover how Financial Independence, Retire Early works, its rules, lifestyle paths, benefits, and challenges so you can plan for early freedom with money.

PERSONAL FINANCE

E.O. FRANCIS

8/19/20258 min read

When I first heard about the FIRE financial theory, I thought it sounded almost too good to be true. FIRE stands for Financial Independence, Retire Early. The idea is simple but powerful: save and invest in a way that gives you enough freedom to leave work decades earlier than the traditional retirement age. What makes this so appealing is the promise of time. Time to do what you want, whether that is travel, spend more days with family, or focus on personal passions. In this post, I will walk you through how FIRE works, the main rules behind it, the different ways people practice it, and the pros and cons you need to know.

Understanding the FIRE Financial Theory

At its core, the FIRE financial theory is about creating enough wealth to live without depending on a paycheck. It combines two ideas: financial independence and early retirement. Financial independence means your investments and savings provide the money you need for daily living. Early retirement means you can step away from full-time work much sooner than most people, sometimes even in your thirties or forties.

The concept is not brand new. It gained real attention in the 1990s through the book Your Money or Your Life. But it exploded in popularity in the 2010s, especially among millennials who began sharing their FIRE journeys through blogs, podcasts, and online communities. The movement now has a global following, with people trading stories about frugality, investing, and building a life on their own terms.

Key Principles of the FIRE Movement

Extreme Saving and Frugal Living

The first thing people notice about FIRE is the extreme savings rate. Many followers aim to save 50 to 75 percent of their income. That sounds intense because it is. To make it work, people cut down on expenses, live below their means, and avoid debt whenever possible.

I once read about a couple who shared their journey online. They lived in a modest apartment, cooked almost every meal at home, and drove used cars long past when most people would trade them in. By living frugally and saving most of what they earned, they reached their FIRE goal years ahead of their peers. The lesson is clear: cutting expenses speeds up wealth building.

The FIRE Number

The FIRE number is the target amount of money you need to retire early. It is usually calculated as twenty five times your annual expenses. This formula comes from the idea that if you only withdraw a small portion of your investments each year, your savings can last a lifetime.

Here is an example. If you spend $60,000 a year, your FIRE number is $1.5 million. That may sound like a mountain to climb, but breaking it down into monthly savings goals and steady investing makes it more achievable. The FIRE number gives you a clear financial finish line instead of leaving retirement as a vague dream.

The Withdrawal Rate and the 4% Rule

Once people reach their FIRE number, they live off their investments. The most common guideline is called the 4% rule. It suggests you can withdraw about 3 to 4 percent of your portfolio each year, adjusted for inflation, without running out of money.

For example, with $1.5 million invested, a 4% withdrawal gives you $60,000 a year. That matches the spending in the earlier example. The rule is not perfect, and market downturns can create risks. That is why many people monitor their expenses closely and adjust withdrawals when needed. The goal is to keep the balance growing even while you are retired.

Investment Strategy

Saving alone is not enough to make FIRE possible. The real power comes from investing. Followers of FIRE usually put their money into stocks, bonds, or low-cost index funds. These investments grow over time and produce passive income through dividends and appreciation.

Think of investing as planting trees. Each tree grows and eventually provides fruit year after year. With enough trees, or in this case enough investments, the harvest can support your life without you needing to work for every paycheck. That is the heart of FIRE: letting money work for you instead of the other way around.

Different Paths to FIRE

One thing I like about the FIRE financial theory is that it is not rigid. People practice it in different ways, depending on their lifestyle goals and tolerance for sacrifice. These paths give flexibility, so you do not have to follow just one strict formula.

Lean FIRE

Lean FIRE is all about living on as little as possible. People who choose this path adopt a minimalist lifestyle, cutting out nearly every expense that is not essential. They may live in smaller homes, rely on public transportation, or avoid eating out altogether.

This approach works for people who value freedom over comfort. It is demanding, but it gets you to early retirement faster since your living costs are low. If you can live happily with very little, Lean FIRE could be your ticket to independence.

Fat FIRE

Fat FIRE is on the other side of the spectrum. Here, the goal is to retire early but still enjoy a comfortable, even luxurious lifestyle. That means a larger home, more travel, fine dining, or hobbies that require spending.

The catch is that Fat FIRE requires a much bigger savings target. Since your expenses are higher, your FIRE number grows too. People who aim for Fat FIRE often have higher incomes or find ways to boost their savings aggressively. The trade-off is more years of work but more comfort in retirement.

Barista FIRE

Barista FIRE is a middle ground. With this path, you reach partial financial independence but still work part-time. The name comes from the idea of working at a coffee shop or another flexible job that brings in income without the stress of a full career.

This option helps people cover health care or extra expenses while still enjoying the freedom of a lighter schedule. Barista FIRE can also be a stepping stone, giving you freedom sooner while you let your investments continue to grow.

Coast FIRE

Coast FIRE takes a different approach. In this version, you save and invest heavily in your early years. Once you build a strong base, you can ease up on savings and “coast” while compound growth does the rest.

For example, someone who saves aggressively in their twenties might reach a point in their thirties where they can stop saving altogether. Their investments will continue to grow enough to fund retirement later, even if they only cover living costs in the meantime. It is appealing for people who want to enjoy life earlier while still planning for the long term.

Benefits of the FIRE Financial Theory

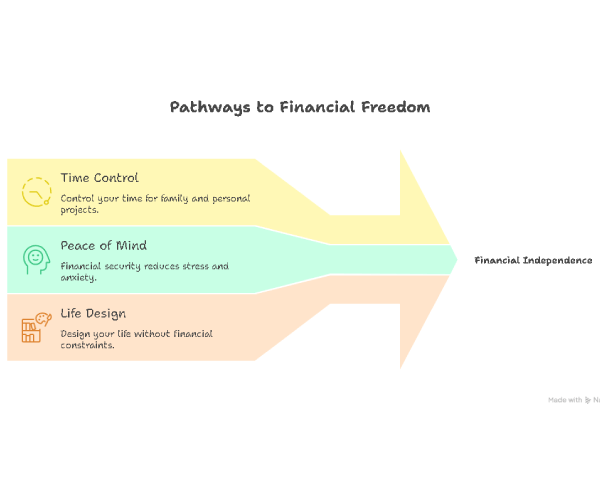

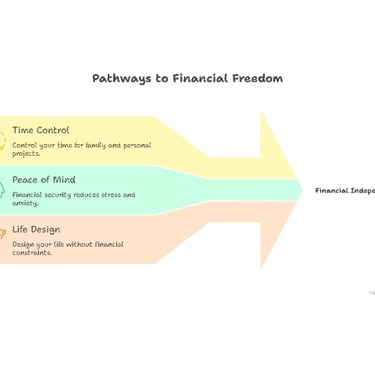

The most obvious benefit of FIRE is freedom. When you no longer rely on a paycheck, you control your time. You can spend your days with family, travel more often, or focus on personal projects that bring joy instead of stress.

Another benefit is peace of mind. Knowing that your finances are secure means less worry about layoffs, medical bills, or rising costs in later years. It creates a safety net that reduces financial anxiety.

FIRE also gives you the ability to design your own life. For some, that means creative work or new hobbies. For others, it means moving to a quiet town, raising children, or volunteering. The point is that you are free to choose without money being the deciding factor.

Challenges and Criticisms of FIRE

Of course, FIRE is not without its challenges. Saving half or more of your income is extremely hard for the average earner. It often means saying no to things most people consider normal, like frequent dining out, new cars, or large homes.

The lifestyle sacrifices can feel restrictive. Not everyone is willing to cut expenses so deeply, and for some, it may affect relationships or social life.

Another concern is investment risk. If markets drop, your savings and withdrawals may no longer cover expenses. That is why constant monitoring and flexibility are key.

Finally, FIRE requires strict discipline and long-term commitment. It is not a quick fix. You need patience and the willingness to stick to your plan even when it gets tough.

How to Start Your FIRE Journey

If you want to try FIRE, the first step is tracking your expenses and income. You need to know exactly where your money goes before you can control it.

Next, look for unnecessary costs you can cut. Even small changes, like cooking at home more often or canceling unused subscriptions, can add up over time.

Increase your savings rate as much as possible. The higher your savings, the faster you move toward independence.

Learning about investing is crucial. Stocks, bonds, and index funds are tools that make your money grow while you sleep.

Finally, calculate your FIRE number. Once you know your target, you can build a plan that guides every financial decision.

Final Thoughts on the FIRE Financial Theory

The FIRE financial theory stands for Financial Independence, Retire Early, and it has changed how many people think about money and work. At its heart, it is about freedom and control of your life.

But FIRE is not one-size-fits-all. Some choose Lean FIRE, others prefer Fat FIRE, and many fall somewhere in between. The right path depends on your income, your values, and the lifestyle you want to live.

If I were giving this advice to a close friend, I would say this: start small, learn the basics, and decide what matters most to you. FIRE is not just about leaving work early. It is about building a life where money supports your choices instead of controlling them.

FAQ

1: What does the FIRE financial theory mean?

The FIRE financial theory stands for Financial Independence, Retire Early. It is a lifestyle and financial plan where people save aggressively, live frugally, and invest wisely with the goal of retiring decades earlier than the traditional age.

2: How do I calculate my FIRE number?

Your FIRE number is the amount of money you need to retire early. The most common formula is to multiply your annual living expenses by twenty five. For example, if you spend $40,000 a year, your FIRE number is $1 million.

3: What is the 4% rule in the FIRE movement?

The 4% rule is a guideline that suggests you can safely withdraw 3 to 4 percent of your investments each year to cover living costs. This withdrawal rate is adjusted for inflation and is designed to make your money last for decades in retirement.

4: What are the different types of FIRE?

There are four popular variations of FIRE:

Lean FIRE: retiring with very low expenses and a minimalist lifestyle.

Fat FIRE: retiring with a higher standard of living and larger savings.

Barista FIRE: semi-retirement supported by part-time work plus investment income.

Coast FIRE: saving heavily early, then letting compound growth carry you to retirement.

5: Is the FIRE financial theory realistic for average people?

Yes, but it depends on your income, expenses, and financial discipline. High earners may reach FIRE faster, while average earners may need to combine strategies like Barista FIRE or Coast FIRE. Even if full early retirement is not possible, practicing FIRE principles can still improve financial security.

6: What are the risks of following the FIRE financial theory?

The biggest risks are market downturns, unexpected expenses, and underestimating how much money you will need in retirement. Living on a strict budget may also feel limiting. That is why people pursuing FIRE must remain flexible and adjust their spending or withdrawals when needed.